Hustler Fund Kenya Explained: Eligibility, Limits, Charges, Repayment, and Better Alternatives

If you’ve heard people talk about the Hustler Fund Kenya and wondered whether it’s actually useful, or just another mobile loan with fine print, you’re not alone. A lot of Kenyans want simple answers: Am I eligible? How do I apply? How much can I borrow? What will it cost me? And what happens if I delay repayment?

That’s exactly what this guide covers.

The Hustler Fund was introduced as a government-backed digital credit option aimed at expanding access to small loans for everyday Kenyans, especially those who may struggle to qualify for traditional bank credit. In practice, it sits in the same decision set as products like M-Shwari, KCB M-Pesa, and Tala, which means you shouldn’t look at it in isolation. You should compare it on the things that matter in real life: eligibility, speed, borrowing limit, repayment period, charges, late-payment consequences, and how easily your limit can grow.

This article takes a beginner-friendly but practical approach. You’ll learn:

- what the Hustler Fund is and why it exists

- Hustler Fund eligibility and basic requirements

- how to apply for Hustler Fund correctly

- how the Hustler Fund loan limit works

- the Hustler Fund interest rates, fees, and total charges in plain language

- how Hustler Fund repayment works and what happens if you miss a payment

- whether using the fund affects your CRB status

- how to increase your Hustler Fund limit over time

- how it stacks up against M-Shwari, KCB M-Pesa, and Tala

One thing to keep in mind: digital loan terms can change over time as providers and regulators update products. So while this guide explains the structure and practical user experience clearly, you should still confirm the latest details inside the official channel before borrowing.

And that matters because even a small mobile loan can become expensive if you borrow casually, roll it over in your mind as “just a little money,” and then miss repayment. The Hustler Fund may be more accessible than some alternatives, but “accessible” doesn’t automatically mean “best” for every situation.

If you want the full picture, benefits, drawbacks, application steps, limits, repayment rules, and alternatives, you’re in the right place.

What Is the Hustler Fund?

The Hustler Fund is a Kenyan government-backed financial inclusion program designed to offer small digital loans to individuals, groups, small businesses, and cooperatives. For most first-time users, the part people mean when they say “Hustler Fund” is the personal loan product accessible through mobile channels.

At its simplest, it’s a mobile-based credit facility that lets eligible Kenyans borrow relatively small amounts directly to their phones, then repay within a short period. The goal is to give people who are often excluded from conventional loans, because of limited paperwork, low income, or thin credit history, a more accessible source of short-term credit.

Unlike a standard bank loan, the process is built for speed and convenience. You typically don’t need to visit a branch, fill out long paper forms, or provide physical collateral for the small personal facility. Instead, access depends on factors such as your identity verification, mobile usage profile, and repayment behavior.

A key feature often discussed is that the fund combines credit access with a savings component on some structures, which was intended to encourage borrowing while also nudging users toward financial discipline. That sounds good in theory. In reality, what matters most to you is whether the product gives you affordable short-term liquidity without trapping you in repeated borrowing.

So, think of Hustler Fund Kenya as a formalized, digital microcredit option sitting somewhere between social-policy financing and commercial mobile lending. It’s not a grant. It’s not free money. It’s a loan product, and you should treat it with the same seriousness you’d apply to any debt.

Why Was the Hustler Fund Introduced?

The Hustler Fund Kenya was introduced to address a very exact problem: millions of Kenyans need small amounts of working or emergency capital, but many can’t easily access mainstream bank credit.

Traditional lending usually favors borrowers with stable payslips, formal business records, collateral, or established banking history. But a huge share of Kenya’s economy is informal. Think small traders, boda boda riders, freelancers, kiosk owners, casual workers, and young adults just starting out. These groups often need modest, fast financing, not a long bank process.

The fund was presented as a way to:

- widen access to affordable digital credit

- reduce dependence on informal and sometimes predatory lenders

- support micro-enterprise and day-to-day hustling

- build a pathway into the formal financial system

- encourage savings and credit discipline

There’s also a political and economic angle. Expanding credit access can be framed as an inclusion policy, especially for lower-income and underserved populations. But policy ambition and user experience are not always the same thing. A loan can be accessible and still feel restrictive if limits are too small, repayment is too short, or users don’t clearly understand charges.

That’s why the Hustler Fund matters most when it solves a real short-term cash need at a cost and repayment timeline you can realistically handle. If it becomes another cycle of borrowing to repay borrowing, then it misses the spirit of financial inclusion.

In short, the fund was introduced to make credit more reachable for ordinary Kenyans, but whether it works for you depends on the details, not the slogan.

Who Can Apply for the Hustler Fund?

The short answer: adult Kenyan citizens who meet the platform’s requirements can apply for the personal Hustler Fund product.

In practical terms, the target audience includes people who are often underserved by traditional lenders, such as:

- informal workers

- small business owners and micro-traders

- self-employed earners

- gig workers and freelancers

- unemployed but mobile-active adults who meet the minimum conditions

- young adults starting their credit journey

This broad target base is part of what makes the product attractive. You don’t need to be a salaried employee with a polished bank statement. But that doesn’t mean absolutely everyone qualifies automatically.

Approval still depends on meeting core conditions such as:

- being a Kenyan citizen

- being at least 18 years old

- having a valid national ID

- having an active mobile line and mobile money profile, depending on the access channel

- meeting internal system checks

This is where many people get confused. They hear “government fund” and assume it works like a universal entitlement. It doesn’t. It’s still a credit product with screening, usage rules, and limits.

If you’re asking whether students or young adults can apply, the answer is often yes, if they’re 18 or older and meet the operational requirements. Employment is not always the decisive factor. But, being eligible to register and actually receiving a meaningful loan limit are two different things.

So yes, the pool of people who can apply is fairly broad. But your actual borrowing experience will depend on how the system assesses your profile.

Eligibility Requirements for the Hustler Fund

When people search for Hustler Fund eligibility or Hustler Fund Kenya requirements, they usually want a clean checklist. Here it is.

To qualify for the personal Hustler Fund facility, you generally need to meet these baseline requirements:

| Requirement | What it means for you |

|---|---|

| Kenyan citizenship | You should be a Kenyan national with valid identification. |

| Minimum age of 18 | You must be a legal adult to borrow. |

| Valid national ID | Your details must be verifiable. |

| Registered mobile line | You typically need an active mobile number linked to your identity. |

| Mobile money access | Access often works through USSD or app-based mobile channels. |

| Compliance with internal checks | The system may assess activity, identity, and risk indicators before giving a limit. |

A few practical notes matter here.

First, eligibility is not the same as approval at a high limit. You may qualify to use the product but still start with a small amount.

Second, if your details don’t match across your ID, SIM registration, and mobile money profile, that can create friction. Even small inconsistencies can affect access.

Third, mobile credit products often rely on behavioral signals. While the exact internal scoring model may not be fully public, factors such as active usage, repayment behavior, and digital financial footprint can influence your borrowing profile over time.

If you’re a beginner, the safest assumption is this: to improve your chance of smooth access, make sure your ID is valid, your SIM is properly registered, your mobile money line is active, and your personal details are consistent.

And one more thing, being eligible doesn’t mean borrowing is automatically wise. If your income is uncertain over the next 14 to 30 days, even a small loan can become stressful fast.

How to Apply for the Hustler Fund

If you want to know how to apply for Hustler Fund, the process is designed to be mobile-first and fairly simple. Exact screens or prompts can change, but the user journey is usually straightforward.

Step-by-step Hustler Fund application process

- Open the approved access channel

This is typically through a designated USSD code or official mobile platform.

- Choose the Hustler Fund option

Follow the menu prompts for the personal loan product.

- Verify your identity details

You may be asked to confirm information connected to your national ID and mobile number.

- Accept the terms and conditions

Don’t skip this blindly. Check the repayment timeline, charges, and any deductions.

- Submit your application

Once the system reviews your profile, it may assign you a starting limit.

- Borrow within your approved amount

If approved, the loan amount is disbursed digitally to your account or mobile wallet, depending on the channel structure.

Tips to apply correctly

- Use your own registered phone line.

- Make sure your ID details are accurate.

- Read the displayed loan amount and repayment obligation before confirming.

- Don’t borrow the maximum just because it appears available.

Common application mistakes

- Using a line not fully registered in your name

- Assuming registration guarantees a large limit

- Ignoring the repayment deadline

- Treating the first approval as a sign that repeat borrowing is safe

The big advantage of the Hustler Fund application process is convenience. The downside is that convenience can make borrowing feel too casual. One minute you’re checking your limit: the next minute you’ve taken a loan you didn’t fully think through.

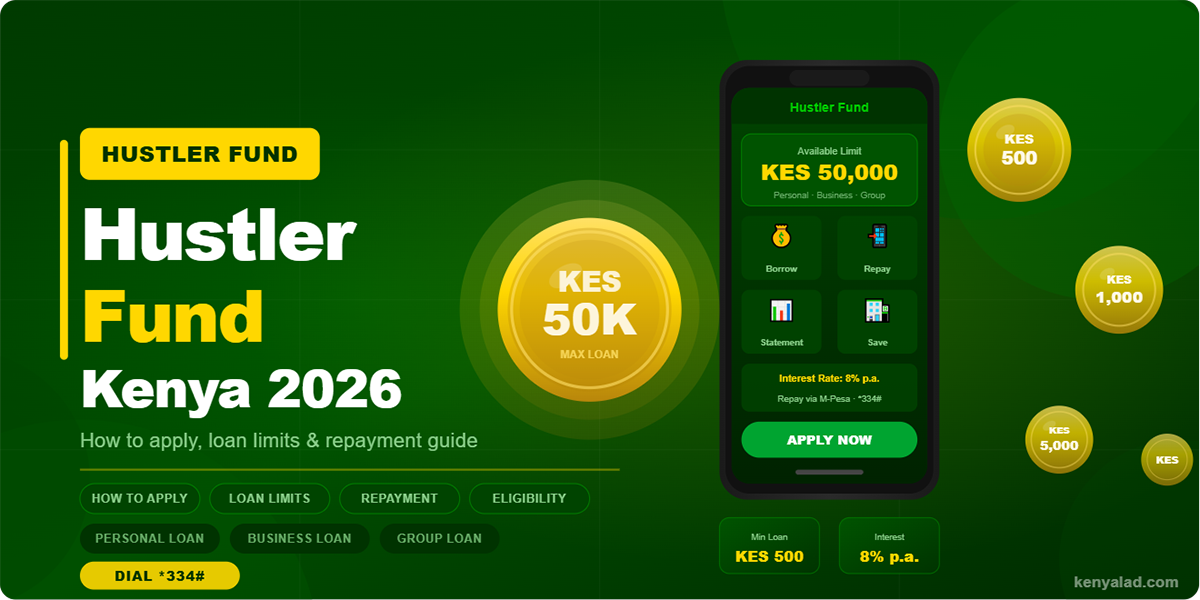

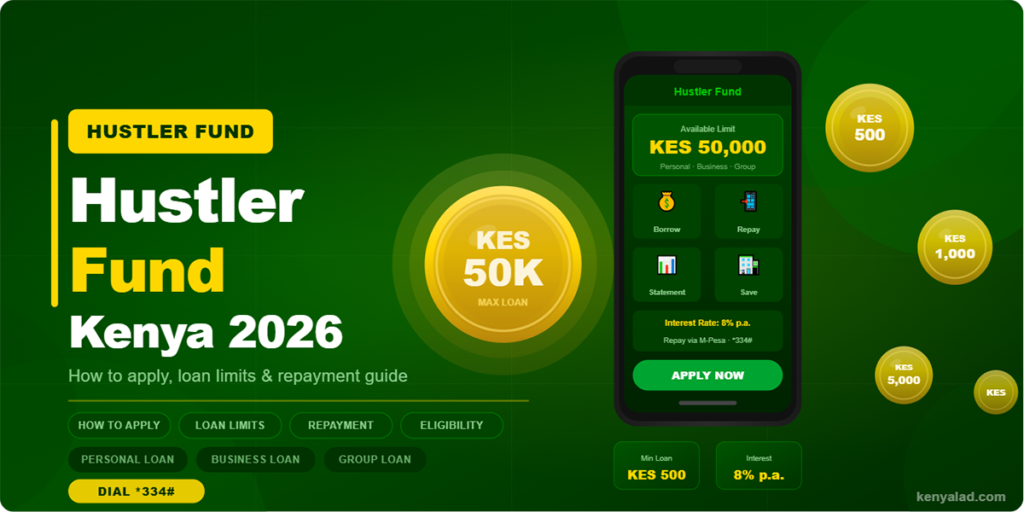

How the Hustler Fund Loan Limit Is Calculated

The Hustler Fund loan limit is one of the most common points of confusion. People want a simple formula, but the reality is that borrowing limits are usually determined by a mix of policy rules and internal scoring factors rather than a single public equation.

In practical terms, your limit is likely influenced by factors such as:

- your identity verification status

- activity on your mobile line

- your mobile money usage patterns

- repayment behavior if you’ve borrowed before

- how consistently you use digital financial services

- broader internal risk assessment criteria

Most new users start with a small initial limit. That’s normal. Mobile lenders rarely begin with their highest exposure because they first want to see how reliably you borrow and repay.

Here’s the key idea: your limit is less about what you say you earn and more about what your financial behavior suggests.

| Possible factor | Likely effect on your limit |

|---|---|

| New user with no prior borrowing history | Lower starting limit |

| Strong repayment record | Better chance of gradual increase |

| Active mobile money usage | Can help signal account activity |

| Inconsistent profile details | Can reduce access or create delays |

| Repeated late payments | May freeze growth or reduce trust |

Some users expect the system to calculate limits like a bank loan officer would, based on salary, collateral, or paperwork. That’s usually not how this type of lending works. It’s digital, automated, and behavior-based.

So if you’re asking how limits are calculated, the honest answer is: through internal scoring informed by your verified identity, digital activity, and repayment conduct. The exact model may not be fully disclosed, but responsible borrowing and on-time repayment are consistently the safest ways to improve your standing over time.

Hustler Fund Interest Rates and Charges Explained

Before you borrow, you need to understand Hustler Fund interest rates and total cost, not just the headline marketing language.

With any digital credit product, your real question shouldn’t be “Is the rate low?” It should be: How much will I repay in total, over what period, and are there any extra charges or deductions?

The Hustler Fund has generally been positioned as a lower-cost alternative to many high-fee mobile loan products. That’s a meaningful advantage. But “lower-cost” doesn’t mean “costless,” and short repayment windows can still make a loan feel expensive in practice if cash flow is tight.

What charges should you look for?

Check for the following every time you borrow:

- stated interest or facility fee

- any administrative charge

- deductions at disbursement, if applicable

- penalties or consequences linked to late repayment

- whether any amount is allocated to savings or retained portions under the product structure

Why the repayment period changes how charges feel

A charge that looks small on paper can feel heavy if you must repay quickly. For example, borrowing for 14 days is very different from borrowing for 30 days or several months. The shorter the term, the more pressure on your next cash inflow.

A practical borrowing rule

Before accepting, ask yourself three things:

- How much will hit my account today?

- How much must I repay in total?

- Can I repay from expected income, not from another loan?

If you can’t answer all three comfortably, pause.

The best way to think about Hustler Fund charges is this: they may be more manageable than some alternatives, but they still require discipline. A “small” digital loan becomes expensive the moment it pushes you into repeat borrowing or late repayment.

How to Repay Your Hustler Fund Loan

Understanding Hustler Fund repayment is just as important as understanding how to borrow. In fact, it’s more important, because repayment is where many borrowers either build trust and grow their limits, or get stuck.

The repayment process is usually digital and meant to be simple. Depending on the active channel, you typically repay through the same mobile network used to access the loan.

Typical repayment flow

- Open the official repayment or mobile money channel.

- Select the Hustler Fund repayment option.

- Confirm the outstanding balance.

- Enter the amount to repay.

- Complete the transaction and keep the confirmation message.

Repayment timeline

The personal Hustler Fund product is generally structured as a short-term loan. That means you should treat it as emergency or working-capital credit, not money for open-ended spending.

Best practices for repayment

- Repay before the deadline, not on the edge of it.

- Keep enough funds in your mobile wallet if auto-collection or payment prompts are part of the process.

- Save transaction confirmations in case of disputes.

- Avoid taking another digital loan to clear this one unless you’ve thought through the total cost.

What if you can’t repay on time?

This is where borrowers often get anxious. Late repayment can affect your ability to access future loans, reduce trust in your profile, and potentially trigger collections or reporting consequences depending on the rules in force.

The smartest approach is brutally simple: borrow only what your next reliable income can clear.

If your repayment will depend on a maybe, maybe sales improve, maybe salary delays clear, maybe a friend sends money, you’re already taking more risk than a short-term mobile loan deserves.

Benefits of Using the Hustler Fund

The Hustler Fund Kenya has some real advantages, especially for people who need fast access to modest credit and don’t qualify easily elsewhere.

Main benefits

- Accessibility: You don’t need a traditional bank-style application process for small personal borrowing.

- Convenience: The mobile-first structure makes access and repayment easier for many users.

- Financial inclusion: It can serve people with limited formal credit history.

- Potentially lower cost than some alternatives: Depending on the product and comparison point, the pricing may be less aggressive than certain digital lenders.

- Opportunity to build a borrowing track record: Good repayment behavior can improve future access.

Where it can help most

The fund may be useful when you need:

- short-term stock money for a tiny business

- transport or work facilitation cash

- a small emergency bridge before expected income

- a way to avoid a more expensive lender

Why borrowers like it

For many people, the biggest appeal is psychological as much as financial: the product feels more reachable and less intimidating than a bank loan. No branch queues, no guarantor drama, no mountain of paperwork.

But the benefit is strongest when the loan solves a exact short-term gap. For example, if KES 800 helps you buy items to sell that same day and you know the cash cycle, that’s different from borrowing KES 800 for impulse spending and hoping things somehow sort themselves out.

So yes, the Hustler Fund can be genuinely useful. Just don’t confuse convenience with harmlessness. Its benefits are real when used strategically, not casually.

Drawbacks and Risks to Consider

A balanced review of Hustler Fund Kenya has to address the downsides too.

Key drawbacks

- Small starting limits: First-time borrowers may find the amount too low for meaningful needs.

- Short repayment window: Even modest loans can feel tight if your income is irregular.

- Risk of dependency: Fast digital borrowing can become a habit.

- Limited flexibility: If you need a larger amount or a longer term, the product may not fit.

- Unclear user expectations: Some borrowers assume a government-backed fund means relaxed repayment consequences. It doesn’t.

Practical risks borrowers overlook

The biggest risk isn’t always the listed charge. It’s behavior.

A mobile loan can create a false sense of safety because the amount looks small. Then you borrow again, or borrow elsewhere to cover it, and suddenly you’ve built a mini debt stack across platforms. That’s where trouble starts.

Another issue is mismatch. If your income comes unpredictably, say, from casual jobs, slow-moving sales, or seasonal gigs, a short-term repayment deadline can hit at exactly the wrong moment.

Who should be cautious?

You should be extra careful if:

- your income is unstable this month

- you already have active mobile loans

- you’re borrowing for non-essential spending

- you don’t know your exact repayment date

- you’re hoping to “figure it out later”

And honestly, “figure it out later” is the sentence behind many bad digital loan experiences.

The Hustler Fund is not automatically risky. But used without a repayment plan, it can still create the same stress found in other short-term credit products.

How to Increase Your Hustler Fund Borrowing Limit

If your starting amount feels too low, you’re probably asking how to increase Hustler Fund limit access over time. While the exact scoring model may not be fully public, the broad pattern is usually clear: limits tend to grow when the system sees lower risk and stronger repayment behavior.

Practical ways to improve your limit

- Repay on time, every time

This is the biggest factor. Consistent repayment signals reliability.

- Avoid partial or late payment patterns

Even when you eventually clear a loan, repeated lateness may slow limit growth.

- Keep your mobile line active

Regular, normal usage can support a stronger digital profile.

- Use mobile money consistently and responsibly

Active transaction history may help build behavioral data.

- Borrow only when necessary

Responsible use matters more than constant use.

- Maintain clean personal records

Ensure your SIM, ID, and account details remain properly matched and up to date.

What won’t necessarily help

- repeatedly checking your limit

- borrowing and repaying in panic cycles

- taking larger loans elsewhere and assuming it boosts this product

- using someone else’s line or inconsistent details

The realistic expectation

Limit growth is usually gradual, not dramatic. Don’t expect to move from a tiny entry limit to a major facility overnight. Think of it like trust accumulation: the system gives a little, watches what you do, then decides whether to expand access.

That may feel slow. But if you’re disciplined, it’s also the safest way a lender can reward reliable borrowing behavior.

Hustler Fund vs M-Shwari

When comparing Hustler Fund vs M-Shwari, you’re really comparing two different styles of digital borrowing.

M-Shwari is closely tied to mobile savings and bank-based digital lending through Safaricom and its banking partner structure. It’s been around longer and is familiar to many users. The Hustler Fund, by contrast, is a government-backed inclusion product aimed at widening entry into formalized credit.

Quick comparison

| Feature | Hustler Fund | M-Shwari |

|---|---|---|

| Provider structure | Government-backed program | Mobile-bank partnership model |

| Access style | Digital/mobile | Digital/mobile inside mobile money network |

| Typical use case | Small short-term borrowing for broad inclusion | Short-term digital loans plus savings behavior |

| Starting accessibility | Often attractive to underserved users | May favor users with stronger mobile money history |

| Savings element | Policy-linked inclusion orientation | Stronger established savings association |

Which is better for you?

Choose Hustler Fund if you want:

- an entry-level digital credit option

- a product designed around inclusion

- potentially simpler access if you’re thin-file or underserved

Choose M-Shwari if you want:

- a more established savings-and-loan environment

- a product many users already understand well

- a structure that may feel more integrated if you already use that network heavily

Watch-outs

M-Shwari can be convenient, but eligibility and limits may still depend heavily on your mobile money behavior. Hustler Fund may feel more accessible, but its short-term nature and small starting limits can be restrictive.

So in the Hustler Fund vs M-Shwari debate, the better option depends on whether you value inclusion and entry access more, or network familiarity and savings-linked usage more.

Hustler Fund vs KCB M-Pesa

The Hustler Fund vs KCB M-Pesa comparison is useful because both are well-known to mobile borrowers in Kenya, but they serve slightly different borrower profiles and expectations.

KCB M-Pesa is a bank-linked mobile lending product that has long been used for quick digital loans and savings. It tends to feel more like a mainstream financial product embedded in mobile channels. The Hustler Fund is more explicitly positioned around inclusion for ordinary Kenyans who need smaller, accessible loans.

Side-by-side comparison

| Feature | Hustler Fund | KCB M-Pesa |

|---|---|---|

| Core positioning | Inclusion-focused government-backed digital credit | Bank-linked mobile loan and savings product |

| User onboarding feel | Broad-access oriented | More bank-structured in perception |

| Loan purpose fit | Small short-term needs | Short-term borrowing with established banking association |

| Limit growth | Tied to behavior and repayment | Also behavior-based, often influenced by account activity |

| Repayment pressure | Short-term | Also short-term, depending on product terms |

When Hustler Fund may be the better fit

- You’re new to formal digital credit.

- You want a simpler, inclusion-driven entry point.

- Your borrowing need is small and immediate.

When KCB M-Pesa may be the better fit

- You already use KCB-linked or banking-linked services comfortably.

- You prefer a product associated with a commercial bank structure.

- You want an alternative within a familiar mobile banking environment.

Bottom line

In the Hustler Fund vs KCB M-Pesa choice, neither wins automatically. Hustler Fund may feel more socially inclusive. KCB M-Pesa may feel more like a conventional digital banking product. Your best option depends on pricing, your approved limit, and how confident you are about repaying on time.

Hustler Fund vs Tala

The Hustler Fund vs Tala comparison is especially important because Tala is often viewed as a dedicated digital lender rather than a public-interest inclusion product.

Tala built its reputation on app-based mobile credit with fast decisioning and behavior-driven underwriting. The Hustler Fund is different in spirit: it is positioned as a government-backed route to broader credit access, especially for borrowers who need smaller sums.

Comparison table

| Feature | Hustler Fund | Tala |

|---|---|---|

| Product identity | Public-interest inclusion loan | Private digital lending app |

| Access channel | Mobile/official digital channels | App-based digital borrowing |

| Borrower appeal | Beginners, underserved users, small needs | Users comfortable with app-based lending |

| Loan size progression | Often starts small and grows gradually | Also behavior-based, with progression tied to repayment |

| Cost perception | Often seen as relatively affordable | Can vary by product and user profile |

Why some borrowers prefer Hustler Fund

- It may feel less commercial and more accessible.

- It can be a good first step into formal digital credit.

- It is often considered when users want to avoid pricier private-lender experiences.

Why some borrowers prefer Tala

- The app experience may feel smoother for some users.

- Dedicated lenders sometimes provide a clearer credit-product flow.

- Repeat borrowers may prefer an network they already know.

Key caution

With Tala or any app-based lender, borrowers should pay close attention to fees, repayment schedule, and consequences of default. With Hustler Fund, the same rule applies, just because it has a policy angle doesn’t mean repayment stops mattering.

In the Hustler Fund vs Tala decision, choose based on total cost, approved amount, repayment realism, and user experience, not just brand recognition.

Common Questions About the Hustler Fund

The most common questions about the Hustler Fund Kenya are usually practical, not theoretical. People don’t just want to know what it is: they want to know how it behaves in real life.

Here are the core takeaways in one place:

- Eligibility: You generally need to be an adult Kenyan with valid identification and a properly registered mobile profile.

- Application: The process is mobile-based and designed to be quick.

- Loan limit: Your starting amount may be small, and growth depends largely on repayment behavior and digital activity.

- Charges: Always check the total repayment amount, not just the headline rate.

- Repayment: It’s a short-term loan, so timing matters a lot.

- Missed repayment: Delays can hurt future access and may trigger additional consequences depending on the prevailing rules.

- CRB concerns: Borrowers should verify the latest policy position, especially as digital credit reporting rules can evolve.

- Students and young adults: If you’re 18+ and meet the requirements, you may qualify, though your limit may be modest.

A useful way to think about the product is this: the Hustler Fund can be good bridge money, but it is usually not good budget money.

Bridge money solves a short, defined gap. Budget money is when you borrow because your month already doesn’t work. That second case is where short-term digital loans become dangerous.

If you use the fund to smooth timing, it may help. If you use it to support a lifestyle or recurring spending you can’t sustain, it can quickly become a pressure point.

Is the Hustler Fund Worth It?

For some borrowers, yes, the Hustler Fund Kenya is worth it. For others, not really.

It’s worth considering if you need a small, short-term loan, you qualify, the total cost is clear, and you already know exactly how you’ll repay it on time. In that situation, the fund can be a practical tool: simple access, modest entry barriers, and potentially better terms than some alternatives.

It’s probably not worth it if:

- you need a large amount

- your income is uncertain

- you’re already juggling other mobile loans

- you’re borrowing for non-essential spending

- you don’t fully understand the repayment deadline or charges

That’s the honest answer. The product is neither a miracle nor a trap by default.

A simple decision test

Borrow only if all four statements are true:

- I understand the total repayment amount.

- I know the exact repayment timeline.

- I can repay from expected income.

- I don’t need another loan to clear this one.

If any of those statements is shaky, step back.

Compared with M-Shwari, KCB M-Pesa, and Tala, the Hustler Fund can be attractive because of its inclusion focus and accessible structure. But the best product for you is not the one with the loudest reputation. It’s the one whose cost, limit, and repayment terms match your real cash flow.

So, is the Hustler Fund worth it? Yes, when used intentionally, for a real short-term need, with a clear repayment plan. Otherwise, even a small loan can become expensive stress.

FAQ Section

What is the minimum and maximum Hustler Fund loan amount?

The exact Hustler Fund loan amount available to you depends on the product rules and your personal limit. New borrowers often start low, sometimes with a modest entry amount, and the maximum available grows gradually for users who repay well. In practice, don’t assume the published top range will be your starting offer. Your actual approved amount is tied to your profile and repayment behavior.

How long do I have to repay the loan?

The Hustler Fund repayment period for the personal loan product is typically short-term. You should always confirm the exact deadline shown during application because digital loan terms can be updated. The safest approach is to treat it as money you must clear from your next reliable income cycle, not from vague future plans.

Can I get another loan before repaying?

Usually, short-term digital lenders want your current loan cleared before full new borrowing access opens up again, though product behavior can vary. If there is any repeat-access feature or partial flexibility, confirm it inside the official channel rather than relying on hearsay. Either way, borrowing again before clearing an existing short-term loan is risky if it creates a debt chain.

What happens if I fail to repay?

If you miss repayment, you may face reduced future access, a frozen or lower limit, collection follow-up, and potential reporting consequences depending on the current rules. Even where the process is less harsh than some private lenders, late payment can still damage your borrower profile. Missing repayment is not just a one-time inconvenience, it can affect what the system trusts you with next.

How can I increase my Hustler Fund limit?

The best way to increase Hustler Fund limit access is consistent on-time repayment. Also keep your registered details accurate, maintain active normal use of your mobile line and mobile money profile, and avoid repeated late payments. Limit growth is usually gradual. There’s rarely a shortcut.

Is the Hustler Fund available to all Kenyans?

Not automatically. The product is intended for broad access, but you still need to meet Hustler Fund eligibility conditions such as age, citizenship, valid identification, and system-based checks. So while many Kenyans can apply, not everyone will receive the same outcome or the same limit.

Does Hustler Fund affect CRB status?

This is one of the biggest borrower concerns. Policies around digital credit reporting and CRB treatment can change, so you should confirm the latest official position before borrowing. In general, missed repayment on formal credit products can have consequences for your financial profile, even if enforcement or reporting frameworks evolve over time. Don’t assume “small loan” means “no record.”

Can students apply for Hustler Fund?

Yes, students can potentially apply for Hustler Fund if they are at least 18 years old, are Kenyan citizens, have valid ID, and meet the operational requirements. Being a student does not automatically disqualify you. That said, approval and loan size depend on your profile, and students should be especially careful with repayment because irregular income makes short-term borrowing harder to manage.

Frequently Asked Questions about Hustler Fund Kenya

What is the Hustler Fund and who is eligible to apply?

The Hustler Fund is a Kenyan government-backed digital credit program aimed at expanding loan access to informal workers, small business owners, and other underserved adults. Eligibility requires Kenyan citizenship, age 18 or older, a valid national ID, an active mobile line, and passing internal system checks.

How do I apply for a Hustler Fund loan and what should I be careful about?

Applications are made via approved mobile channels using a USSD code or app, where you verify your ID and accept terms. It’s important to use your own registered phone line, check the loan amount and repayment terms carefully, and avoid borrowing more than you can repay on time.

How are Hustler Fund loan limits determined and can they increase over time?

Loan limits start small and depend on identity verification, mobile and mobile money activity, and repayment behavior. Consistently repaying on time and maintaining active mobile money use can gradually increase your borrowing limit, but growth is usually slow and based on trust.

What are the repayment terms and consequences of late payments on Hustler Fund loans?

Hustler Fund loans have short-term repayment periods, so timely repayment is critical. Missing payments can reduce future borrowing access, freeze or lower your limit, lead to collections, and possibly affect your credit record. Borrow only what you can repay from your next expected income.

Does borrowing from the Hustler Fund affect my CRB status?

Policies can change, but generally missed repayments on formal loans like the Hustler Fund may impact your credit reference bureau (CRB) status. Always confirm the latest official guidance before borrowing, as small loans do not guarantee exemption from credit reporting.

Can students apply for the Hustler Fund, and is it advisable?

Yes, students aged 18 or older with valid ID and mobile profiles can apply. However, since student income is often irregular, they should be cautious with borrowing and ensure they have a clear repayment plan to avoid stress from the short loan terms.